Releasing the GSEs from conservatorship became a hot topic again this week after President Trump posted that he was giving it “serious consideration” on Wednesday, followed by a Bloomberg interview with Treasury Secretary Scott Bessent on Friday.

The timing of the president’s announcement took many by surprise, given rising bond yields, an uncertain trade war landscape and mortgage rates surpassing 7%. With mortgage rates and bond yields rising, there are understandable concerns that this decision could lead to even higher rates as the year progresses. However, after Besset’s interview, we have some clarity about the future.

First, Bessent said the White House must address trade-related concerns before proceeding with this initiative. Second, a central theme of Bessent’s discussion was that any transition of Fannie Mae and Freddie Mac out of conservatorship must not increase mortgage rates.

What does all this mean for housing? Here’s what I think.

Risks of releasing the GSEs from conservatorship

Over the years, I have discussed the influential role of the GSEs in promoting stability within the mortgage market. Their ongoing conservatorship has provided certainty concerning market health, allowing them to function effectively over the past decade.

This was particularly evident during the challenges presented by COVID-19, where the GSEs played a crucial role in facilitating lending at reasonable mortgage rates and bolstering the American economy. In the early stages of the COVID-19 pandemic, there were concerns among some observers that mortgage lending would become more stringent. While we did experience some tightening in the non-QM (Qualified Mortgage) sector, the fact that Freddie Mac and Fannie Mae were under conservatorship helped prevent widespread credit constraints. This ultimately proved to be a great advantage for the U.S. economy during that period.

I am concerned about the potential consequences of removing government backing from the GSEs. The absence of such support could result in higher mortgage rates, wider mortgage spreads and increased fees. The amount of private capital needed for these two giants would be enormous.

Additionally, during economic strain, the GSEs may face more significant constraints in accessing credit, which deserves thoughtful consideration. During a recession, lenders typically tighten credit to minimize losses, as banks must consider capital requirements. However, in conservatorship, this concern is less significant for the GSEs.

Critically, publicly traded companies have a responsibility to prioritize the interests of their shareholders. Recent events have demonstrated that concerns regarding liquidity can significantly impact bank stocks. This highlights the risk of having Fannie and Freddie publicly traded if the markets go against them.

Also, we could see higher mortgage costs in states impacted by climate change as the risk in those areas would warrant higher pricing for publicly traded companies.

Bessent adds context

Secretary Bessent has raised important considerations regarding the potential increase in mortgage spreads that could arise from the GSEs transitioning out of conservatorship. In the Bloomberg interview he said that if this process would to lead to higher mortgage rates, a thorough reevaluation of the decision to move forward will be warranted.

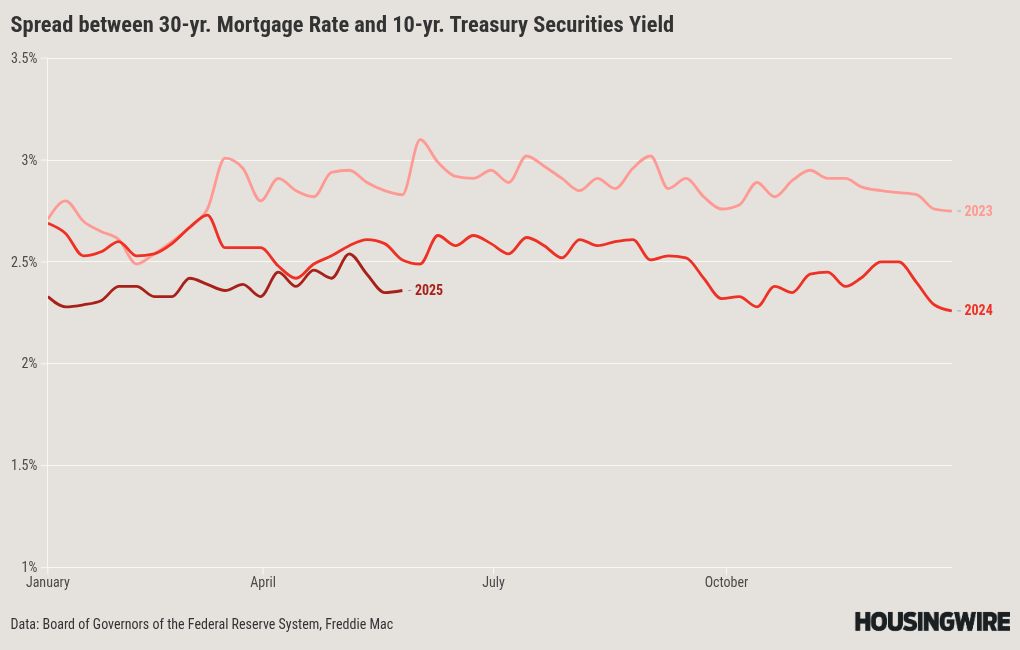

As illustrated in the chart below, mortgage spreads expanded following the Silicon Valley Bank crisis, contributing to the rise in mortgage rates observed in 2023. Indeed, the 8% mortgage rates we experienced during that period could be linked to the deterioration of spreads. At present, mortgage spreads remain higher than historical averages. If we were to return to a more typical environment, we would expect mortgage rates to be closer to 6% rather than 7%. However, if the spreads were to worsen, it’s possible that we could see rates approaching 8%.

After the President’s social media announcement, I was initially concerned about whether the release process might be expedited for reasons we may not yet understand. However, after hearing from Bessent, it seems that the White House is currently focused on other priorities, suggesting there is no immediate urgency to move forward with this plan since the mortgage market is functional already.

I hope this approach holds, as the process to release the GSEs from conservatorship should be thorough and carefully considered to avoid any potential negative implications down the line.

Conclusion

The concerns of real estate and mortgage professionals regarding a GSE release process are valid, especially in light of the elevated mortgage rates we’ve been experiencing. There is a worry that without an appropriate government backstop after an exit, we could end up with higher mortgage rates and less credit availability during a downturn. Many in the housing industry believe that maintaining the status quo is beneficial: as the adage goes, “if it ain’t broke, don’t fix it.”

If we take the Treasury secretary’s statements at face value, it appears that this process will be approached thoughtfully and deliberately.

Engaging with investors will be crucial in assessing the potential impacts on rates, as this is a significant decision that carries long-term implications. Considering the complexities of the current global economic landscape, we must proceed with patience and thorough analysis.

First Time Home Buyer FAQs - Via HousingWire.com