Federal Reserve Chairman Jerome Powell played the Grinch last week for the housing market, sending mortgage rates higher after his remarks at the Fed presser on Wednesday. Despite this, we had positive data on existing home sales, purchase applications, and our weekly pending contract figures. Total active listings are experiencing their traditional seasonal decline, but with less than two weeks left in the year, it’s evident that there are ready homebuyers in America. However, we need lower mortgage rates to grow sales in a bigger fashion in 2025.

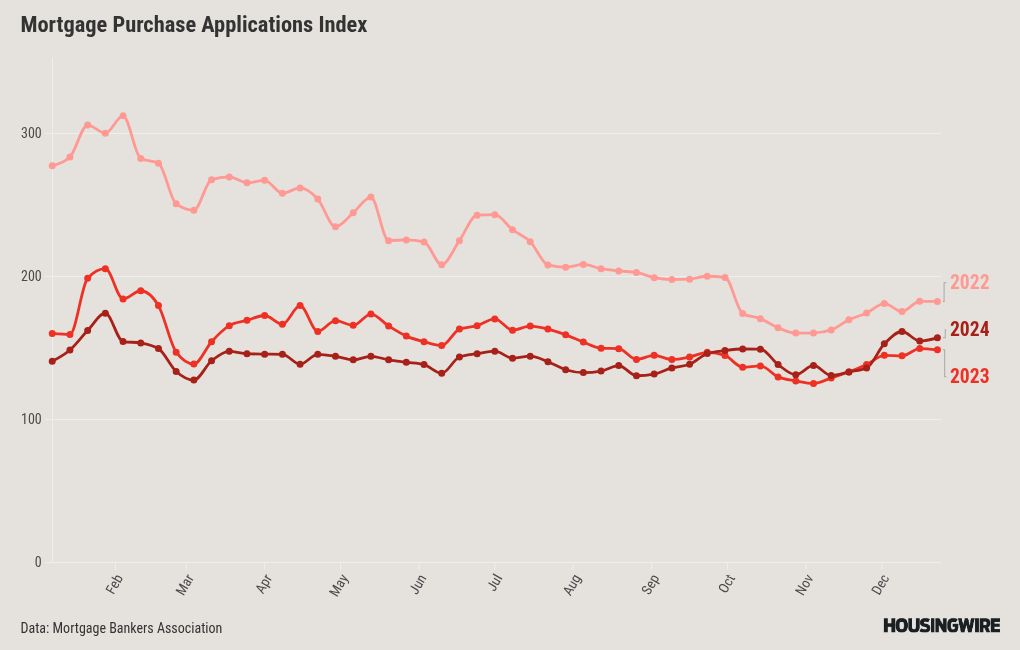

Purchase application data

Purchase application data rose 1% weekly and is up 6% year over year, even with a higher bar to work from. In the last two year,s we have seen an increase in purchase apps in November and December — both times came when mortgage rates fell. However, this year, mortgage rates rose during this timeframe. I believe the seasonal demand in purchase apps is now happening in November and December, which explains the stronger data this year and the last few years as well.

Purchase apps in the last 10 weeks:

- 6 Positive

- 4 negative

The last few weeks have shown a positive year-over-year growth trend, as illustrated in the chart below. I typically disregard the last two weeks of the year, and the Mortgage Bankers Association won’t report those figures until the new year. Therefore, I’d like to conclude that 2024 ended the year slightly positively.

When mortgage rates were running higher earlier in the year (between 6.75%-7.50%), this is what the purchase application data looked like:

- 14 negative prints

- 2 flat prints

- 2 positive prints

When mortgage rates started falling in mid-June, here’s what purchase applications looked like:

- 12 positive prints

- 5 negative prints

- 1 flat print

With the data above on how the market reacted to higher mortgage rates, I can understand some people’s surprise with our Housing Market Tracker data. The last existing home sales report beat to the upside, too; which I wrote about here.

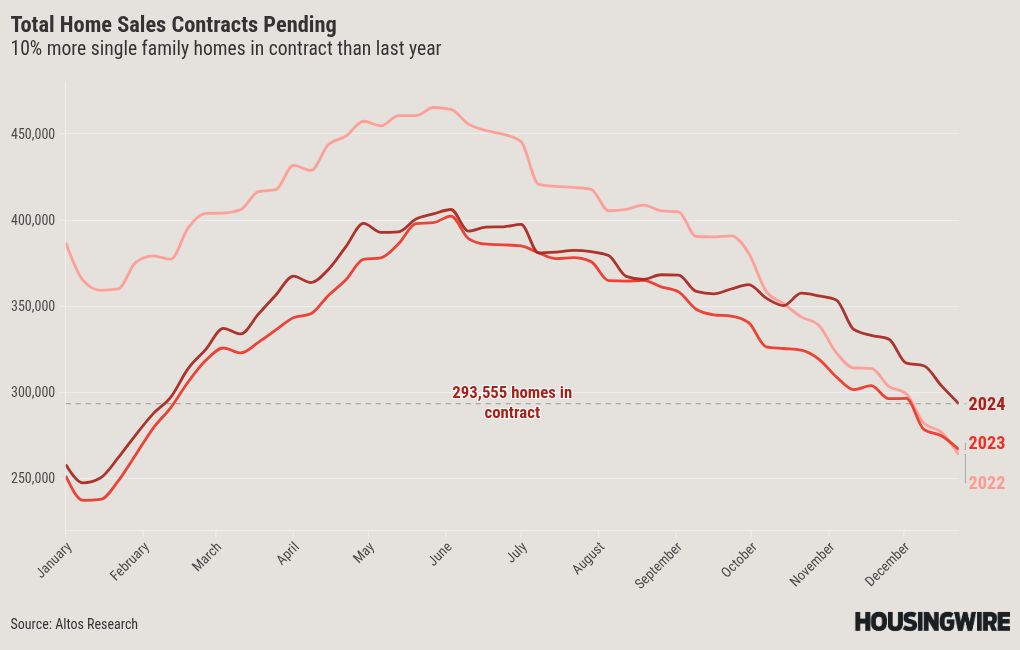

Weekly pending sales

The latest weekly pending contract data from Altos Research offers an exciting glimpse into the real-time dynamics of housing demand. While it’s common to see a seasonal dip in volume at this time of year, there’s a silver lining: we’ve been observing solid year-over-year growth when comparing our data to 2022 and 2023.

This positive trend suggests that despite the typical slowdowns, the housing market is showing some promising resilience as we head toward the end of the year! This is the weekly pending sales for last week over the previous few years:

- 2024: 293,555

- 2023: 267,033

- 2022: 263,937

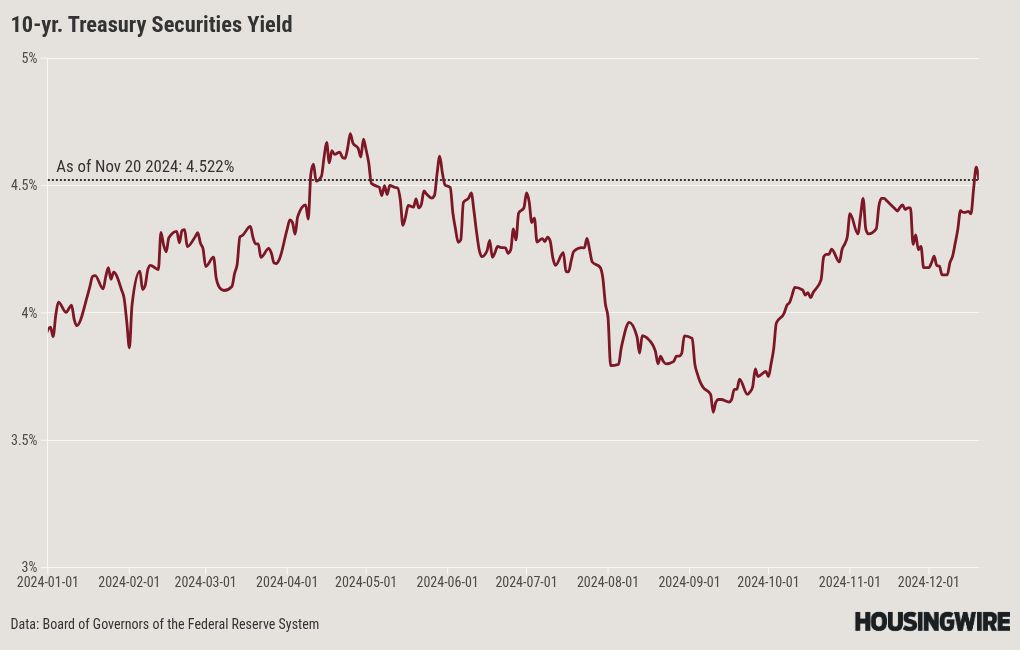

10-year yield and mortgage rates

My 2024 forecast included:

- A range for mortgage rates between 7.25%-5.75%

- A range for the 10-year yield between 4.25%-3.21%

Last week was tumultuous for mortgage rates. Chairman Powell’s statements created a ripple effect in the market. The 10-year yield shot up after the Fed press release and then kept going higher as Grinch Powell talked more.

However, after the inflation report came in softer, bond yields fell and mortgage rates dropped as well. Despite this, it was still a challenging week for both rates and the 10-year yield.

Mortgage spreads

The unsung hero of the housing market in 2024 has been the improvement in mortgage spreads. What was a concerning issue last year has turned into a positive story this year. If mortgage spreads had not improved in 2024, our discussions about housing would be quite different today — especially considering the events of last week.

Mortgage rates would be near 8% if we had experienced the peak negative spreads of 2023. On the other hand, if mortgage spreads were at normal levels, we could expect mortgage rates to be approximately 0.72% to 0.82% lower. Last week demonstrated that even with rising rates, the housing market has fared much better this year than last year, thanks to more favorable spreads.

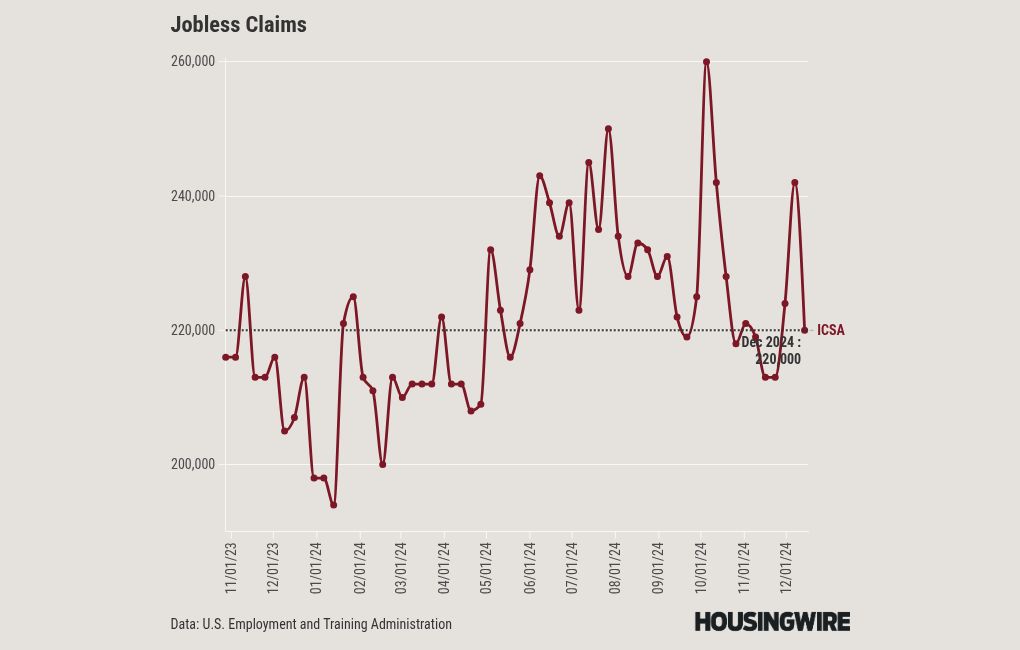

Jobless claims

Jobless claims made a big move lower last week but this weekly data line can get tricky around the holidays. Remember, for my recession indicator to start flashing red, this data line needs to head toward 323,000 on the four-week moving average. This has been my stance since 2022 and we haven’t seen that happen yet. Last week, jobless claims decreased by 22,000 to 220,000. The four-week moving average increased by 1,250 to 225,500.

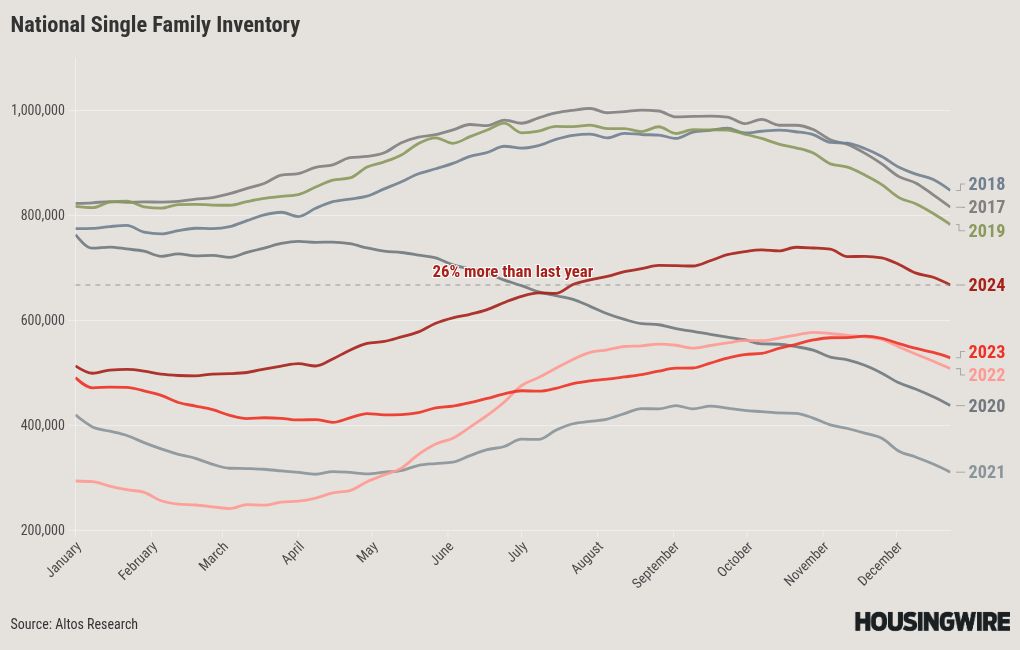

Weekly housing inventory data

As we enter the year’s final weeks, we usually see a drop in housing inventory. However, I’m excited about the story behind the current market — inventory has grown from the depressed levels we experienced in early 2022.

This shift has created a much healthier housing market that has the potential to thrive for years to come. Plus, we can navigate lower mortgage rates without spiraling back into savagely unhealthy conditions. It’s a positive trend that bodes well for the future.

- Weekly inventory change (Dec. 13-Dec. 20): Inventory fell from 682,150 to 667,466

- The same week last year (Dec.14-Dec. 21): Inventory fell from 538,767 to 528,601

- The all-time inventory bottom was in 2022 at 240,497

- The inventory peak for 2024 so far is 739,434

- For some context, active listings for this week in 2015 were 1,013,245

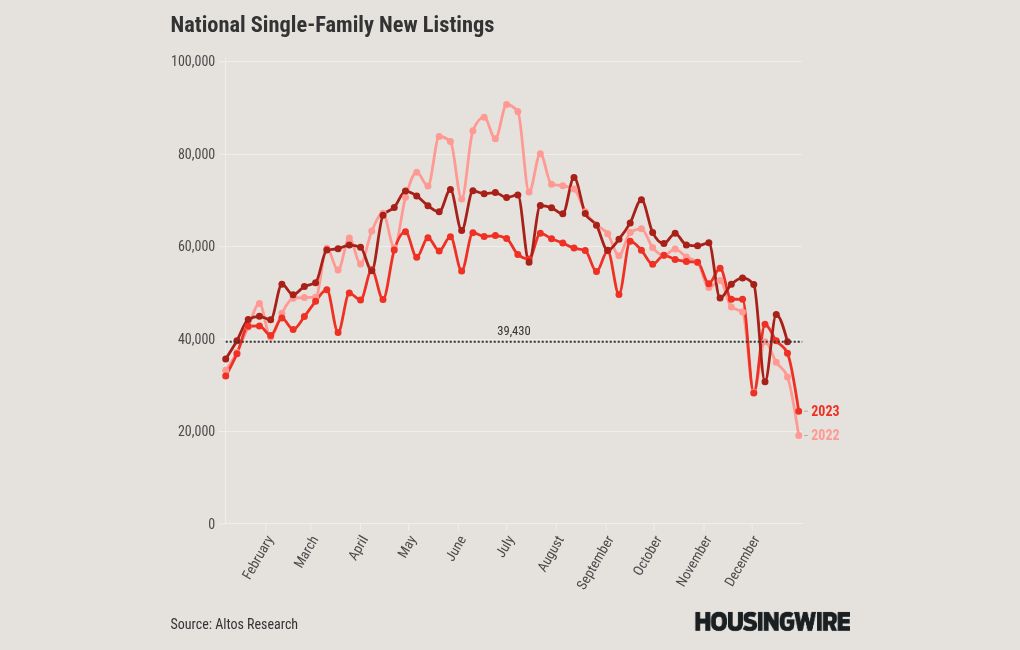

New Listings

New listings data is showing a typical decline for this time of year. Although I didn’t reach my forecast levels this year or the target of 80,000 during the seasonal peak months, I came close, falling short by only about 5,000. I still consider this a positive outcome. Over the last five years, weekly ranges of new listings fell between approximately 30,000 and 90,000. In contrast, during the years of the housing bubble crash, the range was between 250,000 and 400,000.

New listings data for last week over the past few years:

- 2024: 39,430

- 2023: 36,897

- 2022: 31,793

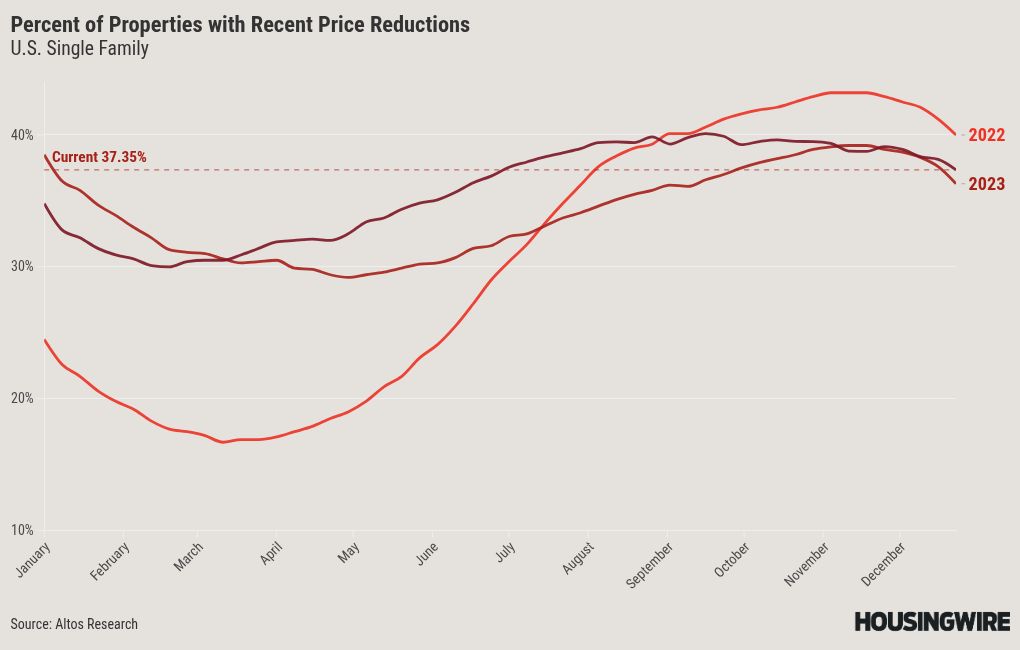

Price-cut percentage

In an average year, it’s common for about one-third of all homes to see a price cut, reflecting the usual dynamics of the housing market. Rising mortgage rates often lead to an increase in the percentage of homes, reducing their prices. On the flip side, when mortgage rates drop, we typically see a rise in demand, which often stabilizes or even boosts home prices, as we’ve recently experienced with falling rates.

My home price forecast for 2024 was a growth rate of 2.33%, but it appears that this estimate may be too low. I initially assumed that the seasonal price softness we typically see in the second half of each year would continue, but recent data shows that home prices have actually firmed up. As a result, my forecast for 2024 may need to be adjusted upward.

Here are last week’s price-cut percentages compared to previous years. Let’s see how this aligns with current market sentiments:

- 2024: 37.4%

- 2023: 36.%

- 2022: 40%

The week ahead: Christmas week and new home sales

Happy Christmas week, everyone! We have the new home sale report coming out this week, which has become an important factor for the economy and the Fed as we look toward 2025. I shared some thoughts on this in my recent article about housing starts. Oh, and don’t forget, we’ll have a few bond auctions happening this week, too! Enjoy the festivities!

Related

First Time Home Buyer FAQs - Via HousingWire.com