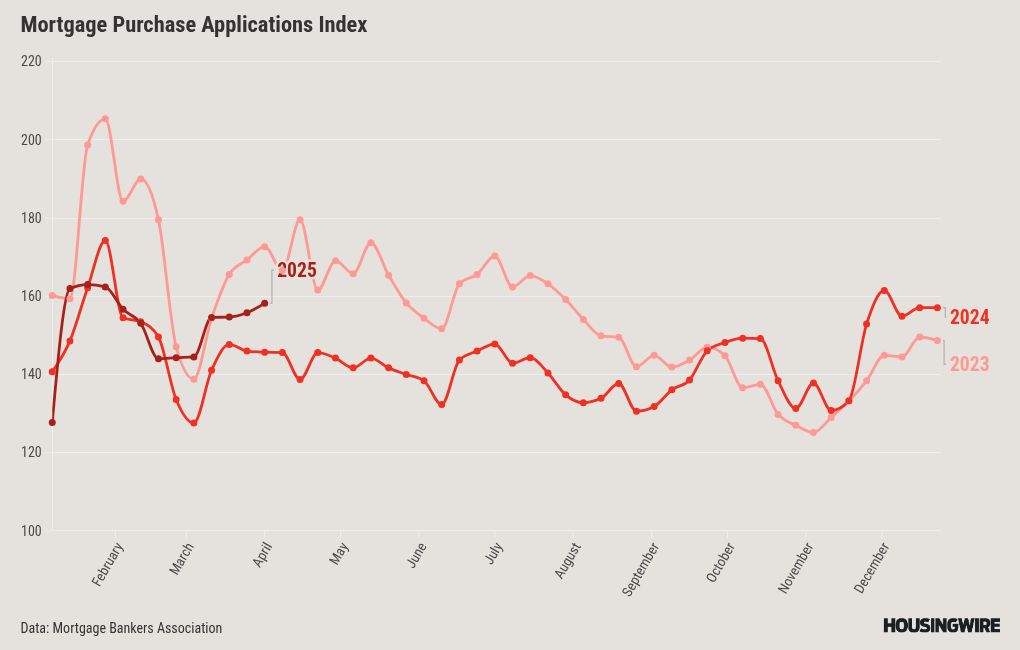

Purchase application data

Mortgage rates hit their lowest point of the year last week, and it’s making a big difference in the key housing data line of purchase apps. Last year, we saw mortgage rates increase from 6.63% to about 7.50%, leading to challenges in the purchase application data. For 18 weeks straight, the trends were mostly not in our favor, with 14 weeks showing a decline week over week. We only had two weeks with positive results and two that were flat. On top of that, there wasn’t any year-over-year growth.

2025 has been much different. Here is the weekly data for 2025:

- 6 positive readings

- 3 negative readings

- 3 flat prints

In general, we have noted encouraging year-over-year growth in most of the weekly purchase apps data for 2025. Last week, we experienced a 9% year-over-year increase. This positive trend has occurred despite mortgage rates remaining above 6.64% until just recently. Traditionally, when mortgage rates dip below this threshold, we have seen data improve beyond typical seasonal patterns as long as it heads toward 6%.

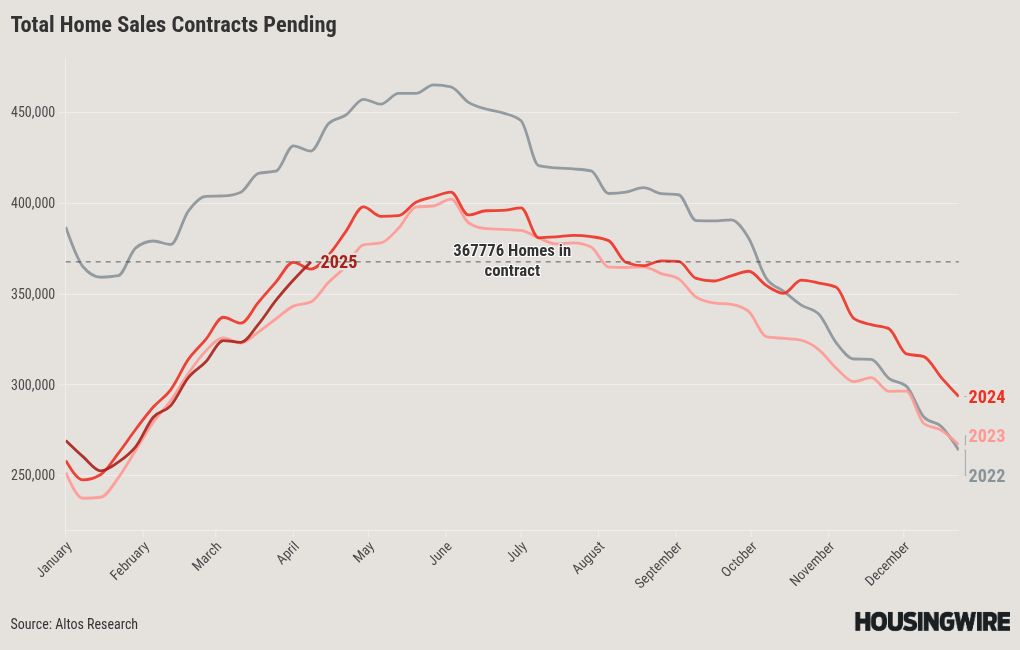

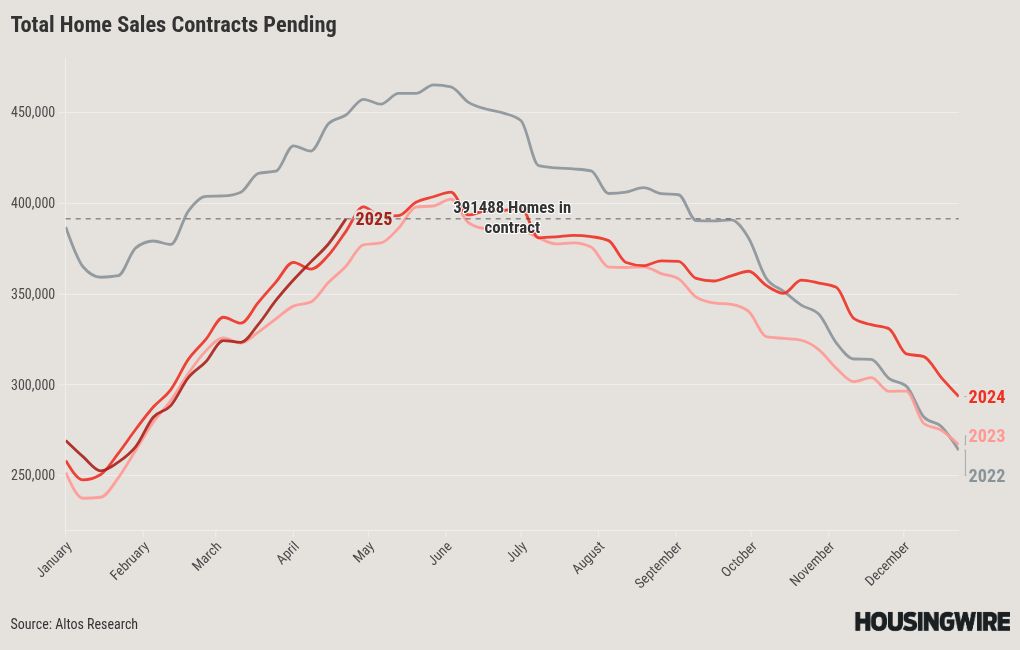

Weekly total pending sales

The latest weekly total pending contract data from Altos offers valuable insights into current trends in housing demand. Usually, it takes mortgage rates to trend closer to 6% to get real growth in the housing demand data lines, but we have recently seen some pick-up on the weekly sales data and now our total pending sales data are positive year over year.

Weekly pending contracts for the last week over the past several years:

- 2025: 367,776

- 2024: 363,834

- 2023: 335,017

For both purchase apps and pending sales, the data presents an interesting trend: the positive weekly figures we’ve been observing coincide with mortgage rates exceeding my growth threshold. Typically, I notice this pattern when mortgage rates decline from 6.64% to 6%. Recently, we did briefly drop below 6.64%.

The key takeaway is that if mortgage rates can continue to trend towards 6% and maintain this duration, we can expect to see an increase in existing home sales this year. This is a point I wasn’t able to address in the past two years, as I would have previously noted that monthly sales data had peaked. As we can see, the outlook for 2025 appears to be different.

10-year yield and mortgage rates

In my 2025 forecast, I anticipate the following ranges:

- Mortgage rates will be between 5.75% and 7.25%

- The 10-year yield will fluctuate between 3.80% and 4.70%

I aim to keep this straightforward. Without the recent tariff developments, the 10-year yield would not have dipped below 4% or approached my low forecast of 3.80% in 2025. During intraday trading last week, we observed a low of around 3.87%. Consequently, mortgage rates have reached a year-to-date low and the market is experiencing notable volatility, largely due to concerns about the potential long-term effects of these tariffs on the economy.

Had the tariffs not been introduced, the 10-year yield would likely be around 4.35% and mortgage rates would be around 6.75%, particularly considering the positive labor reports we received last week. I discuss the jobs report and the various data received here.

I also tried to understand the new tariff plan in this episode of the HousingWire Daily podcast. Any headlines about tariff deals can significantly boost stocks and bond yields, as this would be perceived positively for the economy. Stay alert for breaking news.

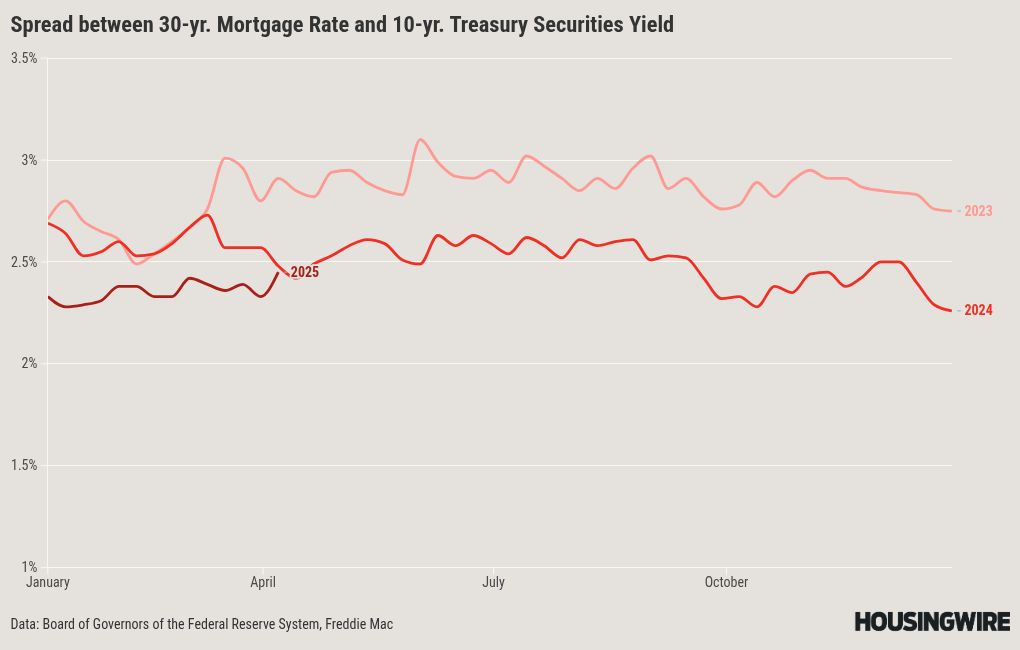

Mortgage spreads

Mortgage spreads started showing positive trends in 2024 and have continued up until last week. With a backdrop of market volatility, the spreads got worse last week. Despite the less favorable spreads, we achieved a year-to-date low in mortgage rates. If we had experienced more typical spreads, we could have rates around 5.75% today, which would be a noteworthy milestone after many years. If mortgage spreads were as bad as the worst levels in 2023, mortgage rates would be around 7.25% today.

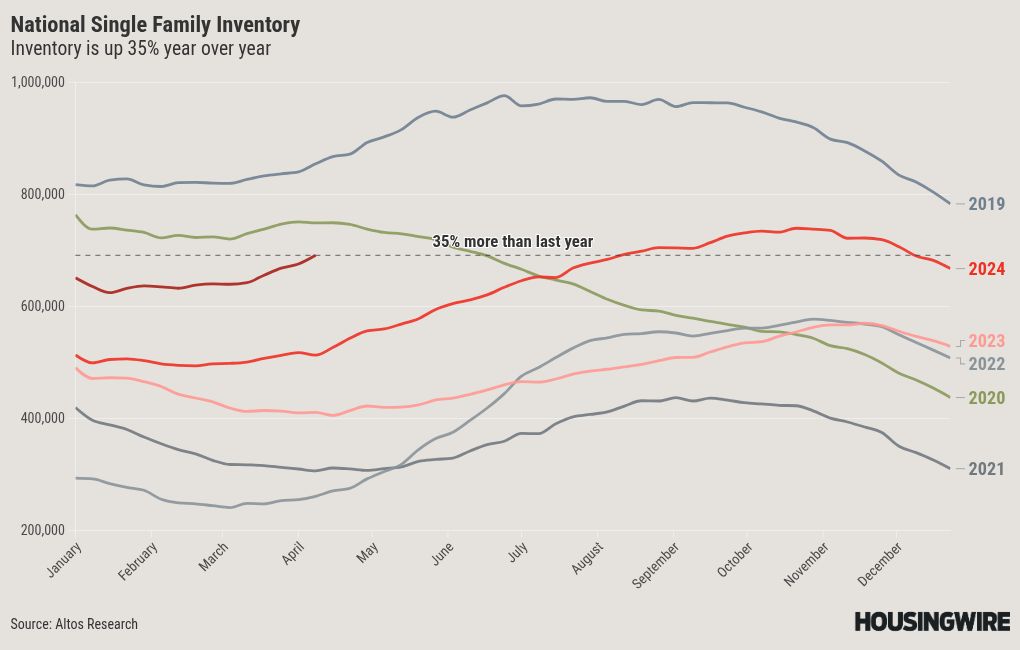

Weekly housing inventory data

Spring is upon us, and for me, the most compelling story in housing for 2024 and 2025 has been the inventory growth. Although we haven’t returned to normal levels yet, I appreciate our progress. Witnessing a solid week of inventory growth brings a smile to my face.

- Weekly inventory change (March 28-April 4): Inventory rose from 675,558 to 691,197

- The same week last year (March 29-April 5): Inventory fell from 517,355 to 512,930

- The all-time inventory bottom was in 2022 at 240,497

- The inventory peak for 2024 was 739,434

- For some context, active listings for the same week in 2015 were 1,021,567

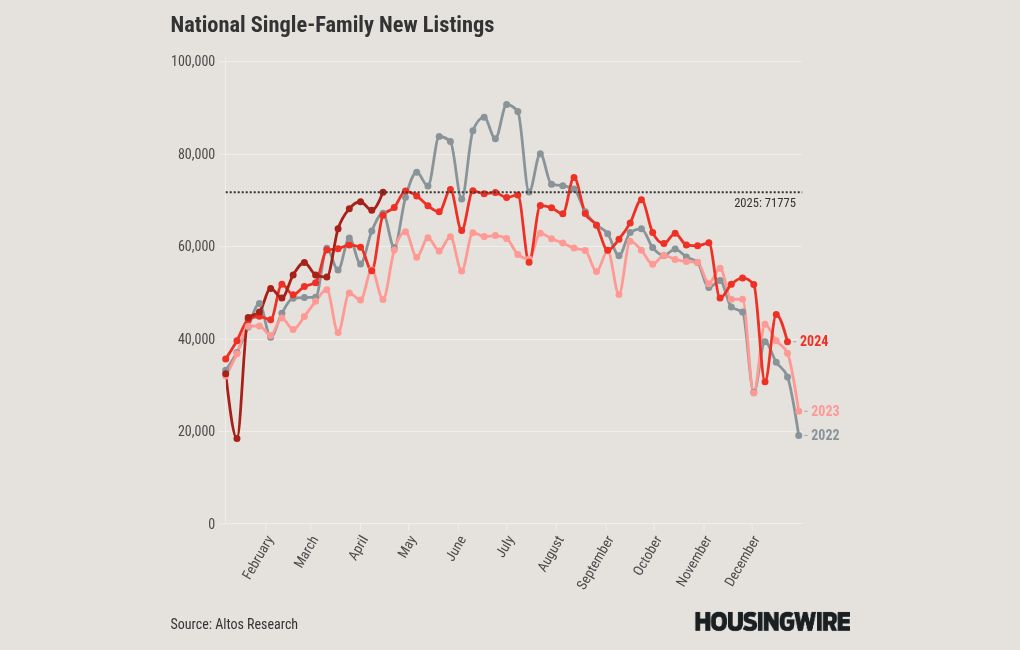

New listings data

The new listings is a bright spot in the housing market today. Last year, I estimated that a minimum of 80,000 homes would be listed every week during the peak seasonal months, and my prediction was only off by 5,000. This year, we will achieve that target: 70% to 80% of home sellers are also buyers and this shift reflects a positive trend as we work towards a more balanced market.

To give you some perspective, during the years of the housing bubble crash, new listings were soaring between 250,000 and 400,000 per week for many years. The growth in new listings data we’re seeing now is just trying to return to normal, where the seasonal peaks range between 80,000 and 110,000 per week. The national new listing data for last week over the previous several years:

- 2025: 71,775

- 2024: 54,769

- 2023: 55,008

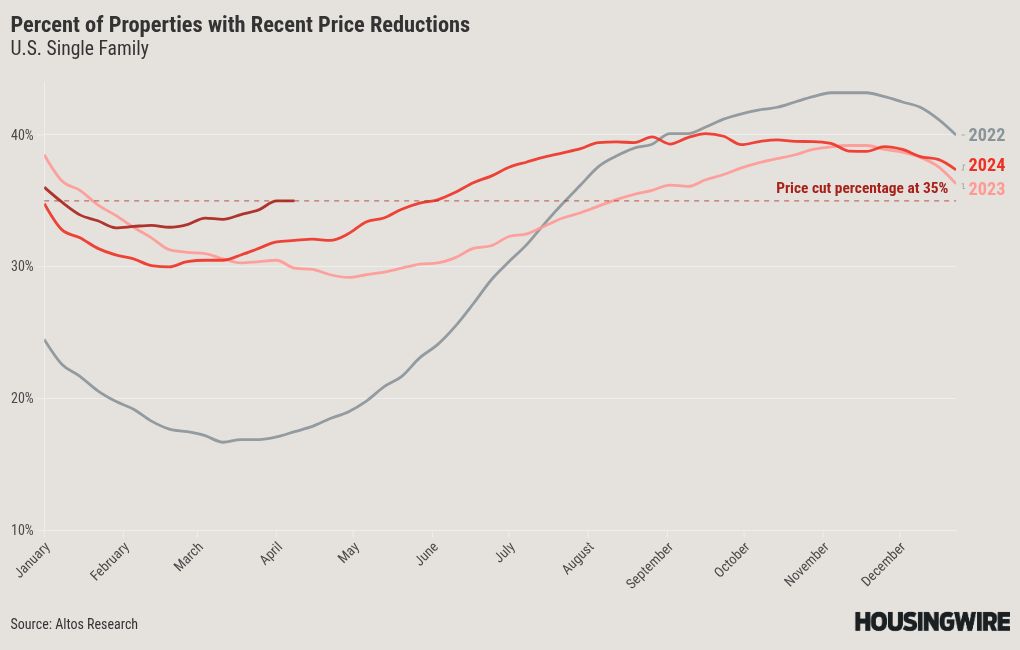

Price-cut percentage

In a typical year, approximately one-third of all homes experience a price reduction, reflecting the housing market’s inherent fluctuations. Given the current rise in inventory levels and comparatively high mortgage rates, the proportion of homes seeing price adjustments has increased compared to times of lower rates. This trend highlights the evolving dynamics within the market.

For the remainder of 2025, I confidently project a modest increase in home prices of approximately 1.77%. At the same time, this suggests another year of negative real home price growth — the current availability of homes and elevated mortgage rates back this outlook. A significant shift in mortgage rates to around 6% could alter this trajectory. My 2024 forecast of 2.33% proved wrong, as lower rates in 2024 made my forecast too low.

The higher percentage of price cuts this year than last strengthens my belief that my conservative growth price forecast for 2025 is well-founded. Price cuts for previous week over the previous several years:

- 2025: 35%

- 2024: 32%

- 2023: 30%

The week ahead: Nothing matters until markets calm down

This week is crucial for CPI and PPI inflation data, and we must closely monitor the speeches from Federal Reserve presidents while tracking these indicators. However, in times of chaos, bond market movements can become extreme. Until the situation stabilizes, this data will have a limited impact. Recently, during jobs week, bond yields dropped significantly, not because of labor data, but due to the prevailing market conditions. Therefore, our attention this week must be on restoring stability to the markets, especially the credit markets.

First Time Home Buyer FAQs - Via HousingWire.com