With sales activity stuck in neutral through the first four months of the year, there’s not much to suggest that the 2025 housing market will be vastly improved from 2023 or 2024. But mortgage leaders and economists are expressing cautious optimism even as the cost of a home loan remains higher than Americans would like.

Data at HousingWire’sMortgage Rates Center on Tuesday shows that 30-year and 15-year conventional loan rates were averaging 6.89% and 6.71%, respectively. The 30-year rate has dropped 6 basis points (bps) in the past week while the 15-year rate is down 11 bps.

Many 2025 housing market forecasts were hopeful that lower rates would’ve arrived by now to accompany the typical peak of the spring purchase season. But economy uncertainty sparked by President Donald Trump’s global tariff policies and resulting fears of rising inflation have kept rates near 7% for much of the year.

Fed effects

The Federal Reserve is unlikely to provide relief on Wednesday when it wraps up its two-day meeting. Interest rate traders are placing 97% odds on the federal funds rate remaining at range of 4.25% to 4.5%, according to the CME Group’s FedWatch tool. About 30% are predicting a 25-bps cut next month.

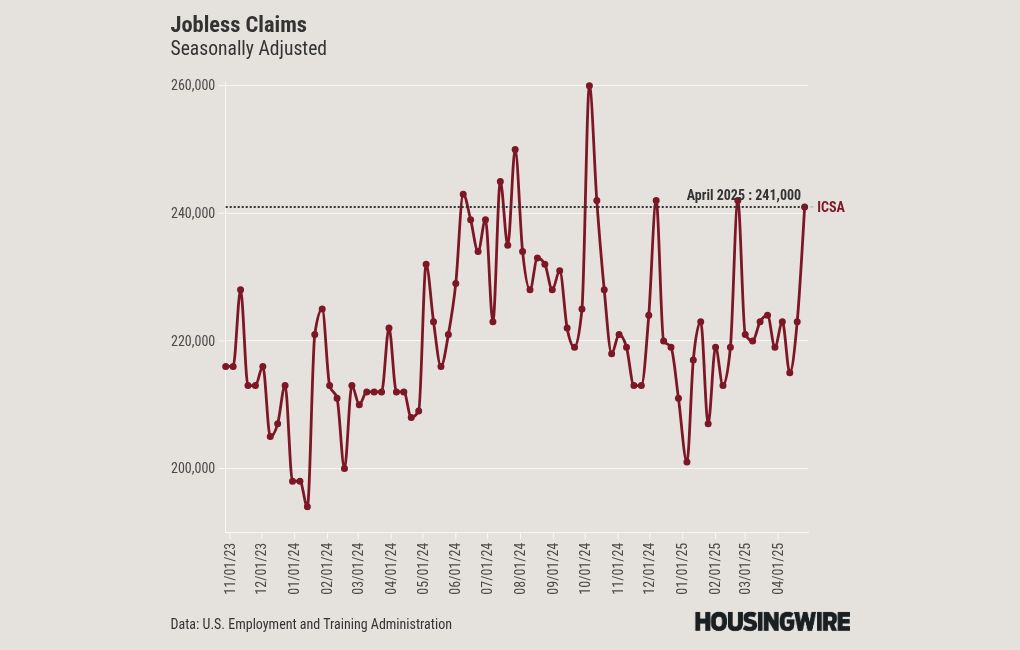

Employers also continue to add jobs at a healthy clip, which serves as a headwind to lower benchmark rates.

“Consumer sensitivity to mortgage rates remains high and rumors of potential homebuyers walking away from their offers in droves dominate the chatter in housing finance,” Selma Hepp, chief economist at Cotality, told HousingWire via email.

“Tariffs and threats to the Fed’s independence all drive uncertainty deeper into the conversation. Rising job losses will define greater mortgage and rent defaults, and while those remain low, there are signs that consumers in lower income ranges are hurting. In addition, consumers are pulling back from spending and adopting a wait-and-see mode which slows economic activity and could kick-start the economy into recession.”

The president has been vocal in his desire for lower interest rates. But while that may be impacting the equity markets, it probably doesn’t give the average American much pause, according to Phil Crescenzo Jr., Southeast division manager for Nation One Mortgage Corp.

“I think that the general public is accustomed to Trump calling anything out he doesn’t fully agree with, so I don’t think this has major effects,” Crescenzo said. “Some may want a shake-up, others may want a cooler temperature. I think the uncertainty overall, in many categories, is causing consumers to be cautious.

“Factors like overtime, that would be an added bonus to income, is relied on in some households, and I’ve seen some cases that the bonuses and extra shifts may not be available, specifically in manufacturing.”

Consumer confidence

Weekly pending home sales were down 10% year over year at the end of April and rose only slightly compared to the usually slow Easter holiday week, according to Altos President Mike Simonsen. And median prices dropped for the first time in nearly two years, although Simonsen was quick to point out that one week does not equate to a trend.

Still, it poses concerns for real estate and mortgage professionals who were counting on favorable economic conditions and more home sales during the spring. And the numerous hurdles to buy a home are reflecting in consumer confidence data as Americans are delaying major purchases, said Samir Patel, senior vice president at Discover Financial Services.

“For a potential housing market rebound in summer, I believe lower interest rates, stabilized inflation and a positive economic outlook would be impactful,” Patel said. “Consumer confidence remains crucial; if measures are taken to increase that confidence then the housing market could regain momentum in the second half of the year.”

Real estate professionals are engaged in an ongoing debate about the rise in private or exclusive listings. This is tied to recent policy shifts from the National Association of Realtors (NAR).

Crescenzo said that “exposure and marketing is still extremely important to get the best price and value,” an indication that a private listing is not the best strategy for every seller.

“I would advise sellers to appreciate buyers, because they are coming in at higher rates and prices, and not try to stretch too far on expectations,” he said. “Be realistic and reasonable to offers that make sense. Offering seller paid closing costs in the form of temporary buydowns is still a valuable strategy we see sellers and their agents offering.”

Mortgage forecast

Some mortgage executives, like Mat Ishbia, remain upbeat and undeterred. In a video posted to YouTube last week, the president and CEO of United Wholesale Mortgage (UWM) — the country’s largest lender — Ishbia pointed to originations estimates from the Mortgage Bankers Association. The trade group’s April forecast calls for purchase and refinance volume to rise from $1.79 trillion in 2024 to $2.08 trillion in 2025.

“Despite continued economic uncertainty and elevated rates, consumers are continuing to live their lives. People are buying homes. People are selling their homes. People are refinancing. People are looking for cash out,” Ishbia said. “More mortgages are going to be done in 2025 than they were in 2024. It’s an opportunity for all of us.”

Victor Kuznetsov, managing director of Imperial Fund Asset Management, indicated that mortgage rates will not change significantly in the foreseeable future. He said the “best-case scenario” is for rates to hover around 6% for the next two years.

“The good news is that employment and home prices remain strong, so families will be in a better position to buy or refinance a home in the coming months, especially if rates dip below 6%,” Kuznetsov said.

First Time Home Buyer FAQs - Via HousingWire.com